Our submissions on the off-payroll consultation

David Kirk & Co. Ltd have made the following submissions to HMRC in response to the off-payroll consultation:

General comments

We believe that making the client, rather than the contractor, responsible for PAYE matters is in general terms the right way to go. However how it is done matters a lot, and with anything as complicated as this there are likely to be side-effects that may turn out to be quite serious and create injustices and a great deal of extra work, in the latter case for HMRC as well.

Regrettably the proposals made in the consultation appear to us to have many flaws in them that will do exactly that, and we believe that a simpler approach is required, that makes the client liable in all circumstances. We understand that this is not favoured by HMRC because it would mean PAYE being operated on the agency’s margin as well as on what the contractor gets. However there is a simple workaround for this which is widely used where agencies make supplies for VAT purposes to clients that are exempt and so have a very similar issue: the agency’s margin is charged separately (and in this instance would not be liable to PAYE), and PAYE could then be operated on the rest of the payment. We believe that agencies would adopt this, and although matters would be slightly more complicated at the client’s end they would be greatly simplified at the contractor’s end, for HMRC when they investigate, and for all parties where there is a default.

Otherwise we have serious concerns about several matters arising:

-

- There will be two off-payroll regimes in place: one for contractors working for small businesses outside the public sector, and another for everybody else. This will not be properly understood by the former group who will have to operate the same rules that on HMRC’s account they are widely ignoring at the moment: the subliminal message that will go out with the introduction of these new rules is that the old ones will no longer apply. This subliminal message will gather extra force when people perceive (as is likely to be the case) that HMRC do not make any serious attempt to enforce the small company rules. Furthermore, when the message has gone out that it is too much of a burden for a small business client to operate the off-payroll rules, it is hard to justify passing responsibility for doing so on to a smaller one (the contractor’s PSC). Finally, unenforceable laws are unfair both on those who keep them and on those ignorant of them that have the misfortune to be caught.

- Those working for small companies will have no mechanism for knowing that they are doing so and therefore have to consider the off-payroll rules. They cannot be expected to look up their clients’ details at Companies House, still less to understand them so as to be able to make the decision, and even if they could there would be no such equivalent for non-corporates or foreign companies.

- There must be a proper appeal system for contractors, in which HMRC are involved and in which end-clients do not have the final word.

- We believe that this reform will result in more off-payroll business being passed to umbrella companies as a means of circumventing responsibility. Whilst we do not see anything intrinsically wrong with that, there are persistent rumours that there a large number of such companies not operating in a compliant manner in the public sector where these reforms have been introduced already (in that they are offering contractor loans which are largely untaxed, which is now flagrantly illegal), and if so this problem can only be expected to spread substantially once they are introduced into the private sector. This is likely to be controversial and the public, Parliament and other branches of Government should be warned about this so that they can take whatever action they feel to be appropriate.

- One other result of the public sector reforms which is virtually certain to be replicated int eh private sector is that clients and agencies quote an ‘umbrella rate’, which is a rate inclusive of employers’ NICs which the worker then ends up paying – or at least perceives that he is doing so. This is the cause of much bitterness and the problem would also be resolved or substantially mitigated by making the client responsible for operating PAYE in all circumstances, as suggested above.

- We remain concerned at HMRC’s track record in defending IR35 cases at the Tax Tribunal, where they have lost ten out of twelve cases since the new tribunal system came in in 2010, and have not clearly won the other two. This suggests that their officers do not understand employment status as well as they should, and is likely to lead to further challenges – this time from people who can afford to take HMRC on which PSCs generally cannot. Any reform is likely to fall flat until this is addressed.

In response to the particular questions:

Question 1 – Do you agree with taking a simplified approach for bringing non-corporate entities in to scope of the reform? If so, which of the two simplified options would be preferable? If not, are there alternative tests for non-corporates that the government should consider? Could either of the two simplified approaches bring in to scope entities which should otherwise be excluded from the reform? Is it likely to apply consistently to the full range of entities and structures operating in the private sector? Please explain your answer.

In our view this would not simplify things – having two different regimes never does. This is only likely to be a problem for sole traders as all other forms of non-corporate, partnerships included, are likely to have balance sheets. We suggest that the matter could readily be dealt with by specifying that if a non-corporate does not have a balance sheet, it is deemed to satisfy the qualifying condition on balance sheets.

Question 2 – Would a requirement for clients to provide a status determination directly to off-payroll workers they engage, as well as the party they contract with, give off- payroll workers sufficient certainty over their tax position and their obligations under the off-payroll reform? Please explain your answer.

Up to a point. It would be very beneficial for the status determination to be required to be given to the worker before he signs the contract, so that he can contest it if he feels it appropriate or walk away from the contract if dissatisfied. Beyond that, it is something that he is likely to find out very quickly anyway, as it will affect the way that he is paid.

Question 3 – Would a requirement on parties in the labour supply chain to pass on the client’s determination (and reasons where provided) until it reaches the fee-payer give the fee-payer sufficient certainty over its tax position and its obligations under the off- payroll reform? Please explain your answer.

No – because the client’s determination might be wrong, even when made after due deliberation and in good faith. If the client determines that the contract is outside the rules, and HMRC disagrees, then HMRC’s recourse is against the fee-payer not the client. This is unjust as the fee-payer is unlikely to have the information to be able to make a decision of this kind without extensive assistance from the client. It will also cause HMRC difficulties as they will have to investigate the client as well as the fee-payer, added to which the client is far more likely than the fee-payer to have the requisite money to pay the shortfall. (Fee-payers exist for the purpose of paying out what they get in, and so generally have very little in the way of reserves.)

Question 4 – What circumstances may result in a breakdown in the information being cascaded to the fee-payer? What circumstances might result in a party in the contractual chain making a payment for the off-payroll worker’s services but prevent them from passing on a status determination?

All the normal failures of office communication could cause this: holidays, key people being off sick, responsibility for making determinations resting in different places from responsibility for hiring. There are also likely to be problems proving that information was passed on after the event: looking for an e-mail with this particular nugget on it on a large company’s server a year later may well be problematic. This is also likely to cause HMRC difficulties as they will need to establish which person in the chain is actually responsible.

Question 5 – What circumstances would benefit from a simplified information flow? Are there commercial reasons why a labour supply chain would have more than two entities between the worker’s PSC and the client? Does the contact between the fee- payer and the client present any issues for those or other parties in the labour supply chain? Please explain your answer.

This would require a major cultural change as generally speaking clients engage agencies to fulfil their requirements, and will expect all communications to go through them – anything else would be seen as a confusing may of managing things. Besides, it is well known that supply chains in the oil and gas sector can be much longer: the specific sectoral reasons for this are not known to us but we can see a genuine role for four intermediaries between the client and the PSC, as follows: client > platform > master vendor > agency > fee-payer > PSC. Where a good many off-payroll workers are required it may be difficult for one agency to supply everybody, so a master vendor would come in to communicate with the client and find the agencies who can supply them. The use of platforms is probably more prevalent in the public sector but there is no reason why they should not be engaged in the private sector as well: they are large well-known companies such as Capita plc who would act in respect of all the client’s requirements, set the general rules and engage with the master vendor.

Question 6 – How might the client be able to easily identify the fee-payer? Would that approach impose a significant burden on the client? If so, how might this burden be mitigated? Please explain your answer.

The only way of doing this is to ask the agency. This would impose a burden but probably not a significant one once agencies became used to providing the information.

Question 7 – Are there any potential unintended consequences or impacts of placing a requirement for the worker’s PSC to consider whether Chapter 8, Part 2 ITEPA 2003 should be applied to an engagement where they have not received a determination from a public sector or medium/large-sized client organisation taking such an approach? Please explain your answer.

We see no chance of this happening in practice – see our comments in section (a) and (b) of General Comments above. We believe that if this reform goes through chapter 8 should be repealed.

Question 8 – On average, how many parties are in a typical labour supply chain that you use or are a part of? What role do each of the parties in the chain fulfil? In which sectors do you typically operate? Are there specific types of roles or industries that you would typically require off-payroll workers for? If so, what are they?

We advise people using supply chains, rather than using them ourselves, and so cannot answer this question.

Question 9 – The intention of this approach is to encourage agencies at the top of the supply chain to assure the compliance of other parties, further down the chain, through which they provide labour to clients. Does this approach achieve that result?

We believe that agencies are inherently unsuitable for this task and that therefore no serious compliance work is likely to be done by them. Many are substantially smaller businesses than their clients and they have neither the skills nor the clout in the market to be able to do this. This might change once a major and costly scandal has hit the headlines but even then we would be doubtful – compliance failures are likely to be seen by most of them as an occupational hazard which it is too expensive to do anything meaningful about. We are also concerned that businesses that were once reputable may cease to be, for instance after a takeover. It is not clear from the consultation document whether the transfer of liabilities is intended to be automatic or discretionary; we believe that if used at all it ought to be discretionary as there will inevitably be circumstances when intermediaries may become insolvent through bad fortune, and others that those responsible for ensuring compliance could not eb expected to pick up. We suggest that any transfer of liabilities be handled by a specialist department of HMRC that is experienced in telling malefactors apart from the genuinely unfortunate, such as exists for transfers of NIC liabilities to directors.

Question 10 – Are there any potential unintended consequences or impacts of collecting the tax and NICs liability from the first agency in the chain in this way taking such an approach? Please explain your answer.

We do not think that agencies are likely to make any serious attempts to protect their position here against unexpected liabilities, which as noted above are likely to be rare and to be seen as unfortunate and unavoidable. Furthermore, a major claim of this kind could well be sufficient to render an agency insolvent – their margins are generally not high. Whilst agencies do have this liability under the agency rules, they have generally dealt with it by either operating PAYE themselves, and thus retaining control over the process, or by insisting on paying through umbrella companies who, having contracts of employment, then have all the PAYE responsibilities themselves.

Question 11 – Would liability for any unpaid income tax and NICs due falling to the client (if it could not be recovered from the first agency in the chain), encourage clients to take steps to assure the compliance of other parties in the labour supply chain?

Not to any serious extent: risks of this kind are not usually seen as being capable of management and so it is always easier to do nothing and accept the consequences. It is difficult to see what assurancesonecangetfromotherpartiesinthesupplychainthatarereallyworthmuch. Where clients do take steps, they are likely to be of a kind where they only use large well-known agencies, thus either adding to the numbers in the supply chain and making it less efficient, or making it difficult for new start-ups to enter the agency world and thus being anti-competitive.

Question 12 – Are there any potential unintended consequences or impacts of taking such an approach? Please explain your answer.

See the answers to the two previous questions.

Question 13 – Would a requirement for clients to provide the reasons for their status determination directly to the off-payroll worker and/or the fee-payer on request where those reasons do not form part of their determination impose a significant burden on the client? If so, how might this burden be mitigated? Please explain your answer.

Yes, but a necessary burden. There is an acknowledged grey area when it comes to employment status, and anyone who suffers adverse consequences from getting status determinations wrong needs to take action to justify and protect his position.

In the private sector the requirement to take reasonable care will need specific legislation and a specific remedy for workers where it is not taken; in the public sector this is by contrast a matter of public law.

Question 14 – Is it desirable for a client-led process for resolving status disagreements to be put in place to allow off-payroll workers and fee-payers to challenge status determinations? Please explain your answer.

No. Clients will largely not have the expertise to resolve marginal cases (which ones where workers are dissatisfied are likely to be) and will hide behind CEST, or if CEST does not give an answer, outsource the issue to specialists who may or may not have the appropriate expertise. Workers are not likely to view them as impartial as the clients will all have an attitude to the risks that they are prepared to take and so may be excessively cautious. It is essential that there be recourse to the Tax Tribunal on this, and that HMRC are involved in the process in some way.

There is a further issue in that some employment status considerations are known only to the worker, such as the number of clients and the nature of the work performed, when the worker claims to be in business on his own account. This is accepted by HMRC (see the Employment Status Manual, pages 549 to 553). It is not generally appropriate that these should be shared with the client (either in relation to the worker’s own affairs or that of his clients), and the client would have no means of knowing whether the worker was telling the truth or not without an exhaustive and intrusive inquiry which most clients would be ill-equipped to carry out. We note in particular with reference to this the FTT’s decision in the recent case of Atholl House Productions [2019] UKFTT 0242 (TC), where this was the criterion for the decision made and the judges, in their section on this (paragraphs 105 to 114), made no reference to the contract at all. It is therefore essential, at least in cases where being in business on one’s own account is claimed to be a factor, that the worker should have direct recourse to HMRC to determine the matter.

Question 15 – Would setting up and administering such a process impose significant burdens on clients? Please explain and evidence your answer.

See our answer to the previous question.

Question 16 – Does the requirement on the client to provide the off-payroll worker with the determination, giving the off-payroll worker and fee-payer the right to request the reasons for that determination and to review that determination in light of any representations made by the off-payroll worker or the fee-payer, go far enough to incentivise clients to take reasonable care when making a status determination?

No, because they will hide behind CEST and so will not have any incentive to engage properly in the process.

Question 17 – How likely is an off-payroll worker to make pension contributions through their fee-payer in this way? How likely is a fee-payer to offer an option to make pension contributions in this way? What administrative burdens might fee- payers face which would reduce the likelihood of them making contributions to the off- payroll worker’s pension?

We do not have the requisite experience to be sure but suspect that the answer would be that there would not be much appetite for pension contributions.

Question 18 – Are there any other issues that you believe the government needs to consider when implementing the reform? Please provide details.

See our answers in General Comments above, in particular paragraphs (d) and (e). Also:

- – There needs to be a deemed employment marker in HMRC’s systems, so that this legislation does not end up getting used by fee-payers to deduct student loan payments or operate pensions auto-enrolment.

- – We recommend that HMRC should make clear what the position is when the OECD Model Tax Treaty is in play. If there is no intermediary, and the client has no tax presence in the UK (unless bearing the cost for a resident party), article 15 specifies that income of someone resident in the foreign state should only be taxed in the UK if that person is in the UK for 183 days or more. In marginal cases – particularly in industries that are project-based, such as construction – the number of days spent in the UK will not be known until close to the year end. If HMRC are expecting a UK-based fee-payer to operate the off-payroll rules irrespective of this, this should be clearly stated.

read more

How to reform IR35, keep the Exchequer in funds, and avoid the hassle that comes with the current private and public sector regimes

On May 18th 2018 HMRC published a consultation document proposing to extend the current public sector regime to the private sector. My own view is that this would be disastrous and unworkable.I do nevertheless have sympathy with HMRC’s view that the current private sector rules areunenforceable and the subject of widespread non-compliance, and feel that – with over 80% ofthe take from IR35 being represented by employers’ National Insurance Contributions (‘NICs’) – some radical change is needed.

This paper, which has been submitted to HMRC, suggest a way forward that ought to get the Exchequer 95% of what it seeks without the hassle and the poisonous feelings that have grown up around the public sector reforms.

Is it possible to consider this?

Basically my proposal is similar to the one at paragraph 6.34 in the Consultation Document, by which the client pays the employers’ NICs and the personal service company (‘PSC’) the employees’. This has been ruled out of scope as ‘it would fundamentally change the NICs treatment of those who would otherwise be within the off-payroll working rules’. I confess that I cannot see why it should. It could be done so that the rules apply equally to the client and to the PSC, just with different parties responsible for paying the various parts (the client the employers’ NI and the PSC the employee’s NI and the PAYE).

The client and the PSC could, of course, take different views as to whether IR35 applied, but if they did so one of them would be wrong. However, bearing in mind that virtually all that was being sought would come from the client, there would be very little in it for the PSC and the worker, as I shall show below. This being so, most of them would comply, and the loss to HMRC where they did not would not be serious.

It would be a less bureaucratic alternative to suggest that IR35 did not apply to the PSC in any event, so that all that happened under this rule would be for the employers’ NI to be collected. This would also raise less money, but only marginally less. It would certainly be true under this alternative that there would be differences of treatment as between the client and the PSC, and it may be that prospect that led the authors of the consultation document to suggest that it should be out of scope. Personally, I cannot see any objection to it on that ground and it would make things simpler for small businesses to deal with their tax obligations. However it is not essential to the operation of this proposal.

Point 1 – the end client must be the liable party, not an intermediary.

This seems to me to be both just and essential in any event, irrespective of whether the rest of the proposal is adopted.

It is just because most of the money raised consists of employers’ NICs: in my estimation about 82%. This is, as its common name suggests, an impost on employers and should be paid by employers (in this instance the clients). Putting the responsibility on to intermediaries allows the employers to ignore their responsibilities here. The idea behind this was that the employers should pay the intermediaries enough to cover the employers’ NI, but I know of no-one who thinks that this actually happens in practice – the issue is simply never raised.

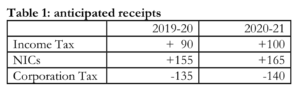

The 82% figure can be gleaned largely from the last Office for Budget Responsibility report, which has the following figures for increased revenue from the new public sector rules. To get there, go to http://obr.uk/data/ and click on Policy measures database, then scroll down to rows 1380 to

1382. I would suggest ignoring the figures for 2017-18 and 2018-19 as it is obvious that it takes time for the full effect of this measure to bring in the full Income Tax receipts. However we see the following for 2019-20 and 2020-21 (in £ millions):

The first point to note here is that the Corporation Tax lost exceeds the Income Tax gained, by quite a substantial margin. As Corporation Tax is a form of income tax paid by companies, and in this case companies owned by people who would be paying Income Tax on the same profits if the companies were not there, it is clear that the measure has not been introduced with this sort of tax in mind. Indeed, as one would expect, the gains come from NICs and easily outweigh the net losses on the income taxes front.

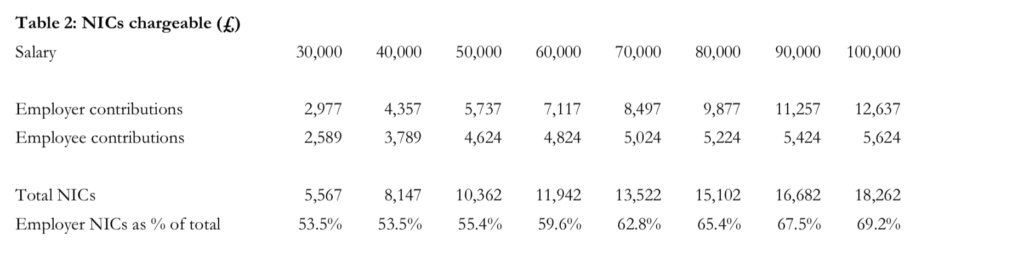

What these figures do not show are the split between employers’ and employees’ NICs, and so I have had to make assumptions here. On the basis that the average deemed salary is £60,000, which would seem to me to be a good working assumption in the absence of any evidence, the proportion is about 60% employers’. As the table below shows, it goes steadily up from 53% on a salary of £30,000 to 69% on a salary of £100,000:

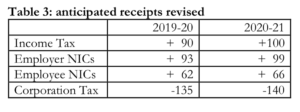

On the assumption then that 60% is correct, this allows us to recalculate table 1 as follows (£ millions):

Or, put more simply:

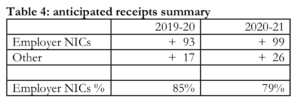

The average is 82%, and in subsequent years it settles down at about this level.

It is essential because otherwise either the employers’ NICs will end up being paid by the worker, which is the source of much unfairness and controversy at the moment, or the intermediaries will resort to avoidance and evasion. The fact is that the intermediaries simply cannot afford to pay the employers’ NICs. At 13.8% on most of the deemed salary, it will be very close to the gross margin (i.e. before overheads) of an agency, and well above the gross margin of an umbrella. If they are to stay in business they need to pass the cost on to someone else. This means that if they cannot charge the client enough to cover it, they reduce the rate paid to the worker. The client obviously has no incentive to pay anything extra, particularly with other agencies being prepared to say that they would take a different view. The only way to make the employers pay is to make them pay directly, not indirectly.

This also avoids the temptation to route payments through non-compliant umbrellas. This I understand to be a major issue in the National Health Service, which has a well-known recruitment problem as it is: it is my understanding that there are some 40-50 umbrella companies, most but not all of them offshore, still paying people though contractor loan schemes, and it is not difficult to see how this happens with these three factors in play:

- NHS trusts (many of which are short of money) refuse to pay any extra to cover the employers’ NI;

- The workers know that they can get higher net pay through umbrellas that give them contractor loans, so they refuse to work for the ones that do not;

- The agencies, unable either to get the NHS trusts or the workers to pay the impost, succumb and contract with these offshore umbrellas. It is likely that in many cases the agency staff would be unaware of what was happening anyway – it is not what they are paid or trained to look out for.

An additional point is that whilst the intermediaries cannot afford to pay this, and the workers see no reason why they should (and often cannot afford it either), many of the clients can absorb the costs without too much trouble. An extra 13.8% on a cost that only amounts to 5% of your total revenue, which will be the case for many enterprises using this sort of contract labour, will put that 5% up to 5.7%, which is unlikely to put the venture at risk, and which they may well be able to recover–atleastinpart–fromtheirclients. Wherethecontractlabourcosts50%oftheirrevenue it is of course another matter, but there will be plenty of cases where this is not so.

If this is a problem in the public sector now, it will be a very much greater one in the private sector if the public sector rules are extended there. The public sector is much smaller and there is more of a compliance culture in it. By contrast, the profit motive in the private sector is likely to come out on top, particularly if businesses can blame someone else for compliance failures.

Added to that, I understand that HMRC are taking action against these non-compliant umbrellas. It obviously remains to be seen how successful this will be, but I do nevertheless have two reasons for being sceptical. Firstly, they are likely to get tripped up when it comes to deciding who the responsible party is. If the worker has a contract of employment with an offshore umbrella, this will be the client (under s. 689 ITEPA), but if not it will be the agency (under s. 44). HMRC will not find it easy to establish the truth as it will have no powers of inquiry vis-à-visthe umbrella, and any attempt to find out from the other party to the contract (the worker) will certainly be time-consuming and probably fruitless. They will therefore be obliged to assume that it is not and challenge the agency to prove otherwise. As most contracts between umbrellas and workers are contracts of employment, their chances of being wrong-footed by an agency that does find out the truth are quite high. With non-compliant onshore umbrellas it will usually be the umbrella that is liable, but there will invariably be no money in it. I suspect that this is going in itself to need legislation to deal with.

It is also worth pointing out that, if found to be on the wrong side of the law, clients are much more likely to pay up than umbrellas or agencies. Intermediaries basically exist to pay out what they get in and rarely have much in the way of reserves (umbrellas in particular). They are more likely to shift their businesses into another company and start again there, leaving HMRC to salvage what little it can from the wreckage.

Thus it can I hope be seen that making the client liable ought to bring three benefits:

- It will prevent the practice of making the workers suffer the employers’ NI;

- It will forestall evasion through umbrellas offering contractor loans;

- HMRC are more likely to recover what they are owed when the law is transgressed.

Point 2 – liability for employee taxes and NICs should remain with the PSC

This means that the PSC would have to operate PAYE on all its receipts under IR35 contracts and pay employee NICs, but not employer NICs as these will have been dealt with already. This has these advantages:

- It prevents arguments. One of the side-effects of the new public sector rules is that there are two industries where relationships between the clients and their workers have become absolutely poisonous, these being broadcasting and the health service. It is no accident that these are industries where staff costs are high as a proportion of revenue and the clients cannot easily afford to pay the extra. However the workers are not locked in a struggle with HMRC about this: they are locked in a struggle with their clients, which is tying up management time to unproductive ends and cannot be good for business in the long run. If the PSCs were left to sort out the employee taxes themselves as well as the clients being left to sort out the employers’, there would be no reason for this and it should all disappear, and with it a great deal of pressure on HMRC who I know are also spending an inordinate amount of time dealing with the problems.

- Administration would be much easier. The PAYE system is simply not designed to collect tax off payments not made to workers directly, and this explains a good deal of the awkwardness that surrounds the current public sector regime. Software would be required that recognised when employers’ contributions were not payable, but this is hardly novel – we have the Employment Allowance already.

- Big business would also find the software much easier. Frequently large companies’ systems are integrated and the introduction of something as complicated as the public sector rules will have knock-on effects. In this instance one has to identify people who are like employees, and so go through the payroll, but are not actually employees, and so do not appear as such in management statistics. They can also be paid VAT, which employees cannot, but on an amount that on the face of it looks incorrect. Leaving big business simply to pay an NI charge on certain contracts, which its software could identify quite easily once the contracts themselves had been identified, would be a great deal simpler. I would hazard a guess that this might enable the reform to be introduced a full year earlier.

- PAYE tax coding would suit the worker and avoid the need for extra tax to be paid through SA returns, or for refunds to be made. Currently unless the fee payer gets a P45 it is supposed to use the BR code, which will lead to the wrong amount of tax being paid – generally an underpayment.

Additional paperwork

Any additional paperwork will be unwelcome, but one piece is essential here which I believe will be simple to operate and far easier to understand than the current public sector system. The client will need to give a certificate to the next in the chain to say that IR35 is being operated, and the next in the chain will be required to issue a certificate to that effect to the next, and so on until one gets to the PSC. This will have two effects:

- It will authorise the PSC not to pay employer’s NI contributions on any salary up to the amount on the certificate; and

- It will at the same time put the PSC on notice that the client is applying IR35. The PSC will therefore need to have good grounds not to do the same. HMRC would be able to have regard to the fact that the client had issued a certificate when investigating the PSC, and I would expect the Tax Tribunal to take it into account as well in any subsequent action in that forum.

There would need to be penalties for failure to pass these certificates on, and it would help if there were incentives to do so as well. As between the client and the agency, one possible way of doing this would be to allow the agency to get a rebate for employer’s NICs paid on sums that exceed the amount paid to the PSC. For example, if the client pays the agency £100 and the agency pays the PSC £85, then the client will have paid £13.80 in employers’ NICs on a deemed salary of £85, a rate of 16.2%. If the agency could claim back the NICs on the differential (£2.07 in this instance), this would give it the incentive to get the certificate from the client, as well as providing an automatic mechanism for getting the employer NICs paid at the right rate on the right amount. I would also expect the market to work in this instance, so that agency margins were reduced to compensate.

As between the agency and the PSC, it would probably be necessary for the agency to get confirmation from the PSC that it has received the certificate and to be able to refuse to pay until it does so.

Possible objections

Objection no. 1 – the client pays NICs on a higher sum than the deemed salary paid to the worker.

This is because of the agency’s margin, as noted in the previous section. My preferred solution would be the one suggested in that section, but an alternative would be to charge NICs at a lower rate where IR35 is in play. If one works on an average agency margin of 14%, the rate would be 11.9% instead of 13.8%.

Objection no. 2 – the client has to work out which contracts are paid through PSCs and which are not.

There may be other off-payroll workers paid through umbrellas or directly by the agency. The short answer is that clients have to do this now in public sector cases – the only difference will be that they will have to pay the employers’ NI themselves where IR35 applies, but will have to give the agencies enough money for parties down the chain to pay it where the agency rules apply or where an umbrella has a contract of employment with the worker.

If this is an issue (and I do not see why it should be – agencies are quite adept now at collating the requisite information about how people are paid further down the chain), it might be worth considering extending this regime to agency worker cases as well. This would resolve a number of problems in the agency sector, which has many of the issues described above too.

It would in turn however necessitate distinguishing cases where the SDC test applies (for agency workers) from those where the normal employment status test does (in PSC cases). The result would generally be the same anyway, but again, if this is considered an issue, it might be worth while standardising the entire intermediary sector around the SDC test, which would certainly be simpler to operate.

Objection 3: the PSC might take a different view.

As noted above, it would be doing so on notice that it was taking a different view, and so much more aware of the risk that it was running than it is now, where many PSCs do not perceive any risk at all. If the certificate were to include a statement that that the PSC was recommended to show it to the company’s accountants or tax advisers – a statement that could be made mandatory – most of their accountants would become aware of the issue too: something that is conspicuously lacking at the moment. All this would encourage compliance.

However I suggest that the most likely factor to encourage compliance would simply be that it would not be all that costly to comply. It would also be administratively easier, in that payment of tax would all be done through PAYE not long after the money is received, and not through and combination of Corporation Tax and Income Tax a long time after. Although it would mean paying tax earlier, many PSC owners would prefer that if it means that they do not have to keep track of large liabilities looming many months ahead.

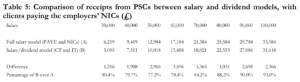

The table below shows the difference in taxes paid by the PSC and the individual as between a full salary model and a salary/dividend model.

Using the £60,000 average once again, this would mean that with a compliant client and a non- compliant PSC, HMRC would receive:

- All of the employer’s NICs (82% of the total due)

- 78% of the 18% due from the PSC (14% of the total due).

Thus even if all PSCs failed to comply, HMRC would still receive 96% of the sums due to them.

It would be untrue to say that nobody would consider these differences to be too small to be worth forgoing the money, but many would think that, when they weighed in factors such as ease of administration and the risk of being found non-compliant, they would prefer to use the PAYE model.

Objection 4: this does not deal with the problem of income splitting.

Income splitting is a set-up whereby the PSC is not wholly owned by the worker, but some shares are also owned by his spouse. This enables him to divert dividends (but not salary) to that spouse and so double up on the personal allowance, the dividend allowance and the basic rate band. This was found to be legitimate by the Supreme Court in Jones v Garnett [2007] STC 1536.

I do not see this as a major problem. This was widely used in the days when wives did not do paid work, but that is comparatively rare nowadays. It is only of any real use where there is a serious disparity of earnings as between the two, and very rarely of any use except where the lower earning spouse earns substantially less than the top of the basic rate band. Also it is my experience that, even where it might be of benefit, people are reluctant to ‘give’ their earnings to their spouses in this way, for reasons of retaining control over those earnings.

Objection 5: this does not take account of people stacking up their profits in their PSCs and not distributing them.

It is possible to avoid Income Tax altogether (paying only Corporation Tax) by drawing from one’s PSC only sufficient to pay one’s living expenses, and saving up the rest in the company. The plan would be to liquidate the company when the worker has no further use for it and pay Capital Gains Tax on the final distribution, claiming Entrepreneurs’ Relief and so paying CGT at 10%. Otherwise only Corporation Tax is paid on the profits.

Despite the propensity of some parts of the press to draw attention to this possibility, in my experience very few PSCs do this: most people need the money to live on. I do not therefore see this as a major problem.

Objection 6: this does not deal with the problem of PSCs that get incorporated and then never file anything

Under this type of evasion the PSC receives all the money from the contract, pays it out to the worker, and never files any further paperwork with either HMRC or Companies House. The result is that the company gets struck off the register after little more than a year, and well before HMRC realise that there is anything that needs investigating there. If the worker still has any use for a company, he will set up another one and repeat the process.

This is not particularly an IR35 problem, and in my experience the only sector where I have seen it in operation at a serious level is construction. Paradoxically, not much money is likely to be lost to HMRC in this sector because of the Construction Industry Scheme, which is a good antidote to this. It is nonetheless very difficult for someone without access to HMRC’s figures to estimate how serious this is. It is, though, a flagrant example of evasion of tax, and will not appeal to people who are prepared to indulge in avoidance but draw the line at evasion. If it is perceived to be a serious problem, the solution is that suggested and discarded on paragraph 6.36 of the consultation document (a withholding tax similar to that operating in the construction industry). This would be very bureaucratic and is not recommended unless substantial sums outside the construction sector are at stake.

Conclusion

In summary, I recommend this model for serious consideration. The first part – placing responsibility on to the client rather than intermediaries – seems to me to be essential in order to make the private sector roll-out leak-proof. The second part – leaving responsibility for the employee taxes with the PSC – would be much easier to operate, would reduce the lead time for introducing it, and would remove a great deal of the political heat from the scene in exchange for leaving the Exchequer with a very small, and certainly manageable, loss of tax.

read more